Crypto License in Panama

€4,500

- Unregulated Legal Crypto Activities

- Global Access

- Register your crypto company in up to 2 weeks

- 0% Corporate Tax Rate

- No Capital Requirements

Under Markets in Crypto-Assets Regulation, a single authorization in any one EU Member State gives CASPs EU-wide “passporting” rights — get authorised once and operate across all 27 countries.

This article is brought to you by the team at AdamSmith. AdamSmith is a team that helps crypto companies establish and maintain legal structures in 20+ countries.

Please note: none of this information should be considered as legal, tax, or investment advice. While we’ve done our best to make sure this information is accurate at the time of publishing, laws and practices may change. For help with the legal structuring of your project, speak to us.

MiCA (Markets in Crypto-Assets Regulation, Regulation (EU) 2023/1114) is the European Union’s new legal framework that harmonises rules for crypto-asset service providers (CASPs) and issuers across all 27 member states. Existing virtual asset service providers may benefit from national transitional regimes until 1 July 2026, after which MiCA authorisation will be required to operate in the EU. Under MiCA, CASPs such as exchanges, custodians, and crypto-brokers must meet strict requirements on governance, safeguarding of client assets, IT security, and disclosure. Authorisation in one EU country gives firms “passporting” rights to serve clients across the entire Union.

Sources: ESMA (European Securities and Markets Authority), Official Journal of the European Union (OJ).

Unlike national VASP registrations, MiCA creates a single authorisation regime across all 27 EU member states. It applies to issuers of Asset-Referenced Tokens (ARTs), issuers of E-Money Tokens (EMTs), and CASPs such as exchanges, custodians, brokers, and trading platforms. Authorisation in one member state gives “passporting” rights to operate throughout the Union.

MiCA does not apply to financial instruments governed by MiFID II (e.g. securities, shares, derivatives) or to fully decentralised protocols with no identifiable issuer. These fall under other EU or national regulations.

National Competent Authorities (NCAs). Authorise CASPs in their home Member State and supervise ongoing compliance. Scope includes governance, safeguarding of client assets, IT/outsourcing, disclosures, marketing practices, and enforcement (information requests, inspections, sanctions, suspension/withdrawal of authorisation).

ESMA (EU-level coordination and transparency). Promotes supervisory convergence through guidelines and technical standards, coordinates cross-border matters, and maintains the EU public register of authorised CASPs and their passporting notifications.

EBA (stablecoins and prudential focus). Leads on prudential expectations for significant ART/EMT issuers (e.g., reserves, liquidity, recovery/wind-down planning), working with NCAs and ESMA.

ECB and national central banks (financial-stability input). Provide opinions and participate where relevant for significant tokens, focusing on monetary policy and payment-system implications.

Entry into

the force of MiCA

Entry into

application

of MiCA

MiCA becomes

mandatory for

service providers

Transitional

phase ends

MiCA replaces fragmented national registrations with a single authorisation. Once your CASP is authorised by its home NCA, you can “passport” services across all 27 EU countries; your authorisation and passporting notices appear in ESMA’s public register (useful for banks and partners).

Regulators expect real decision‑making in the EU (place of effective management) and at least one director resident in the EU—not a letter‑box set‑up. ESMA/EBA guidelines also emphasise time commitment, competence and clear roles for the management body and qualifying shareholders.

If you receive client fiat (other than e‑money tokens), you must place it with an EU credit institution or a central bank by the end of the next business day, and never use client assets for your own account. Expect segregation, daily reconciliation and clear custody contracts—plus liability where a loss is attributable to you.

Trading platforms must monitor market abuse, keep complete order/traceability records, and publish pre‑ and post‑trade data (near real‑time; free after a short delay such as 15 minutes and kept available for 2 years). Keep order‑book data ready for supervisors for years and formalise best‑execution.

For tokens other than ARTs/EMTs, the offeror must be a legal person and draw up, notify and publish a crypto‑asset white paper before public offering or admission—unless a narrow exemption applies (<150 persons per Member State, or ≤€1m over 12 months, or qualified‑investor only). Retail buyers get a 14‑day withdrawal right if they purchased before trading starts. If a token has no identifiable issuer (e.g., BTC), the platform/person seeking admission shoulders disclosure and warnings.

“Algorithmic” models do not qualify as ARTs/EMTs under MiCA. Asset‑backed issuers face strict reserve quality, 1:1 backing, liquidity and disclosure requirements; EMTs link to a single fiat and follow an e‑money‑style regime. Only the issuer (or a party with its written consent) may publicly offer or seek admission. Significant tokens trigger stricter EBA‑coordinated oversight.

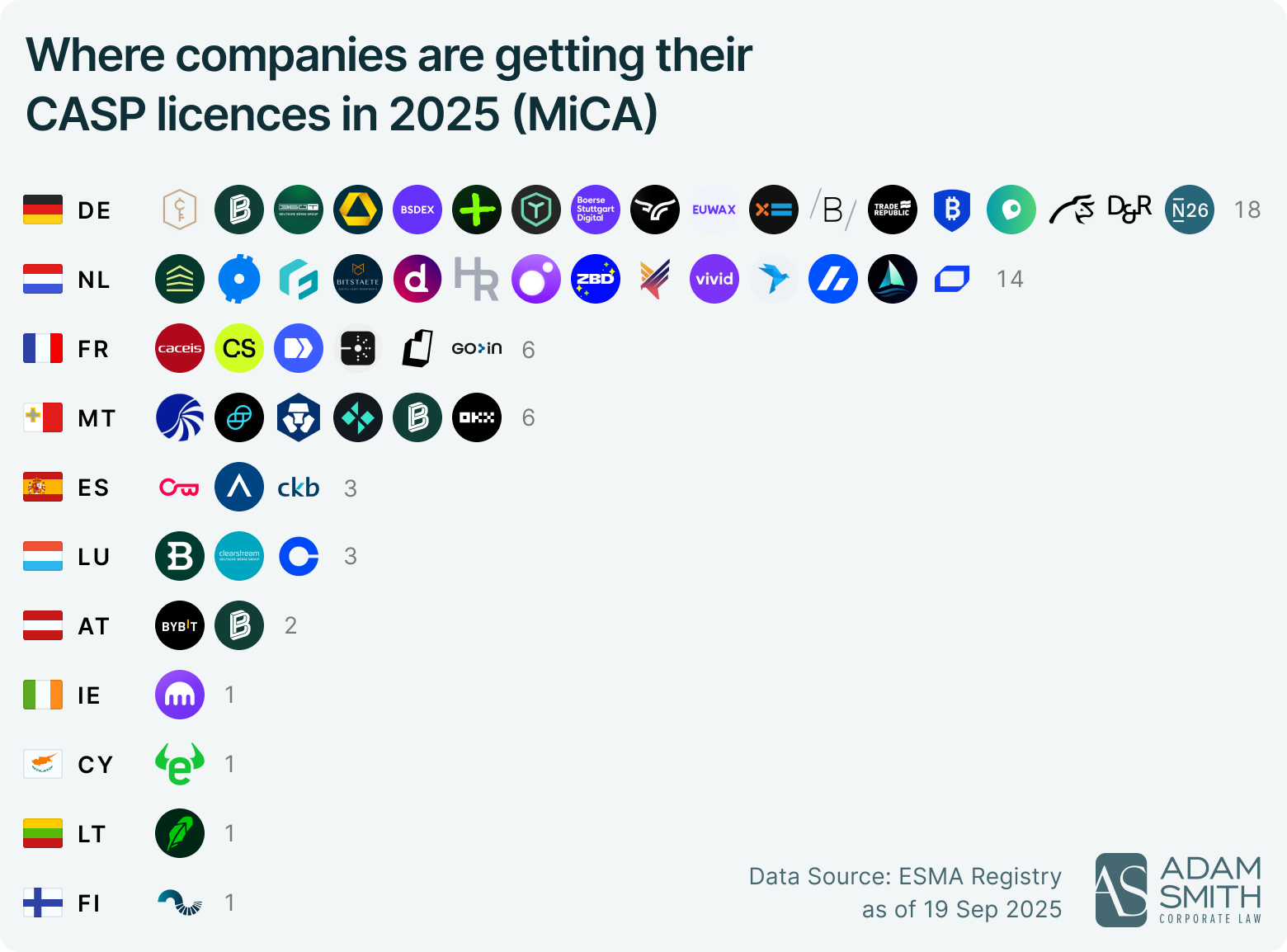

57 unique CASPs across 11 Member States are in the register.

Top home states: Germany (18) and Netherlands (14) lead; then France (6), Malta (6); Spain (3), Luxembourg (3); Austria (2), Ireland (2); Cyprus (1), Lithuania (1), Finland (1).

First-wave approvals landed on 30 Dec 2024 in the Netherlands (BitStaete, Hidden Road Partners, MoonPay, Zebedee).

Peak months for new entries in 2025: May–July (steady flow of large names and banks).

Infographic: Where companies are getting their CASP licences in 2025 (MiCA)

Germany: a cluster of regulated banks and broker-banks (Commerzbank, flatexDEGIRO Bank, Baader Bank, N26, Trade Republic) plus custodians (BitGo, Tangany) and the Boerse Stuttgart group. If you want bank-grade optics and deep capital‑markets links, Germany is where many incumbents went.

Netherlands: strong crypto‑native and payments mix (Bitvavo, Amdax, MoonPay, Finst, Fiat Republic, Acheron Trading) and several first‑day approvals. Good for on/off‑ramp and brokerage‑style models.

Luxembourg: global brands with rapid passporting (Coinbase, Bitstamp, Clearstream). If you need fast EU‑wide reach with a capital‑markets friendly home, this is the pattern.

Malta: large exchanges (OKX, Crypto.com, Gemini, ZBX, Bitpanda) — a clear “trading/exchange hub” narrative.

Plus France (CACEIS Bank; CoinShares AM), Spain (BBVA, Openbank, Cecabank), Austria (Bybit, Bitpanda), Ireland (Kraken), Cyprus (eToro), Lithuania (Robinhood), Finland (Coinmotion).

Firms that safeguard private keys or manage client crypto-assets (similar to custodians or wallet providers)

Providers that run order books or trading venues for crypto-assets

Companies that facilitate exchange between crypto and fiat or between different crypto-assets

CASPs that execute trades or transfers on behalf of clients

Firms that market or distribute new crypto-assets on behalf of issuers

Providers that transmit client instructions to other CASPs or venues

Entities that manage crypto portfolios for clients

CASPs giving personalised recommendations

What happens: choose the Member State and National Competent Authority (NCA), incorporate the legal entity, and establish “substance”.

Baseline expectations:

What happens: informal engagement with the NCA to confirm the service perimeter (custody/exchange/execution/venue, etc.), use of any transitional regime (if already operating), class implications, outsourcing approach and documentation set.

Outcome: aligned scope and expectations, which reduces later rounds of requests for information (RFIs).

Core dossier contents:

Submission: the dossier is filed with the NCA (Day 0).

Acknowledgement: typically within 5 working days.

Completeness check: up to 25–30 working days.

Possible outcomes:

What the NCA assesses:

Process: 1–3 RFI rounds, occasional interviews or remote system walk‑throughs.

Timing: MiCA foresees a decision within 40 working days from completeness, extendable by +20 working days where clarifications are requested; in practice, assessment typically takes 3–6 months from submission.

Decision: authorization or refusal. Upon approval, the firm is listed in ESMA’s public register; passporting notifications are then filed to serve other Member States.

Next steps: align T&Cs and marketing to the authorised status; keep register information current.

What banks/payment providers request: the authorization letter, board minutes, full policy set (especially safeguarding/AML), proof of reconciliations and segregation, and the UBO/KYC pack.

Result: operational accounts are opened and services begin under the MiCA regime.

We handle the entire MiCA authorization process for fixed fee

With extensive experience in licensing crypto companies since 2016, our team has successfully guided numerous businesses through complex regulatory landscapes, helping them achieve compliance and operate confidently within the European market.

MiCA (Markets in Crypto-Assets) is an EU regulation that sets clear rules for Crypto-Asset Service Providers (CASPs), ensuring transparency, investor protection and market stability across all 27 EU member states.

All CASPs operating in the EU, including crypto exchanges, wallets, trading platforms and token issuers, must obtain a MiCA license to provide services legally.

MiCA will be fully implemented by December 2024, with a transition period extending into 2025 for compliance adjustments.

A MiCA license grants legal access to the EU market, enhances credibility, ensures regulatory protection and enables seamless operations across member states.

MiCA requires €50,000 for advisory services, €125,000 for custody and exchange and €150,000 for trading platforms. These thresholds ensure financial stability and regulatory compliance based on the CASP’s risk levels.

Under the MiCA regulation, (CASPs) must be licensed by their national authority, meet governance and capital requirements and comply with strict conduct, AML/KYC, and cybersecurity rules. They must safeguard client assets, provide transparent risk disclosures and follow fair trading and best execution practices. Ongoing obligations include reporting, record keeping and ensuring any outsourcing arrangements remain under full CASP responsibility.

The licensing process varies by country, but typically takes 3 to 6 months, depending on the business structure, documentation and regulatory approval timeline.

MiCA licenses are issued by national financial regulators in each EU member state, following ESMA guidelines.

Yes, a MiCA license obtained in one EU country allows a CASP to operate freely across all 27 member states without additional licensing.

CASPs operating without a valid MiCA license may face heavy fines, operational restrictions, or a ban on services in the EU market.

Yes, MiCA covers stablecoins, utility tokens and security tokens, requiring issuers to meet specific disclosure and reserve requirements.

ESMA oversees the implementation of MiCA, sets regulatory standards and ensures harmonization across EU financial markets.

Yes, but non-EU companies must register a legal entity in an EU country and meet all regulatory and compliance requirements.

Typical requirements include a business plan, AML/KYC policies, risk management framework, cybersecurity measures, governance structure and financial statements.

We provide full regulatory support, including consulting, application preparation, document drafting, communication with regulators and ongoing compliance assistance to ensure a smooth licensing process.

Your application has been successfully sent!

We will contact you within a few business hours.

In case of urgent questions, you can contact us by phone or email: